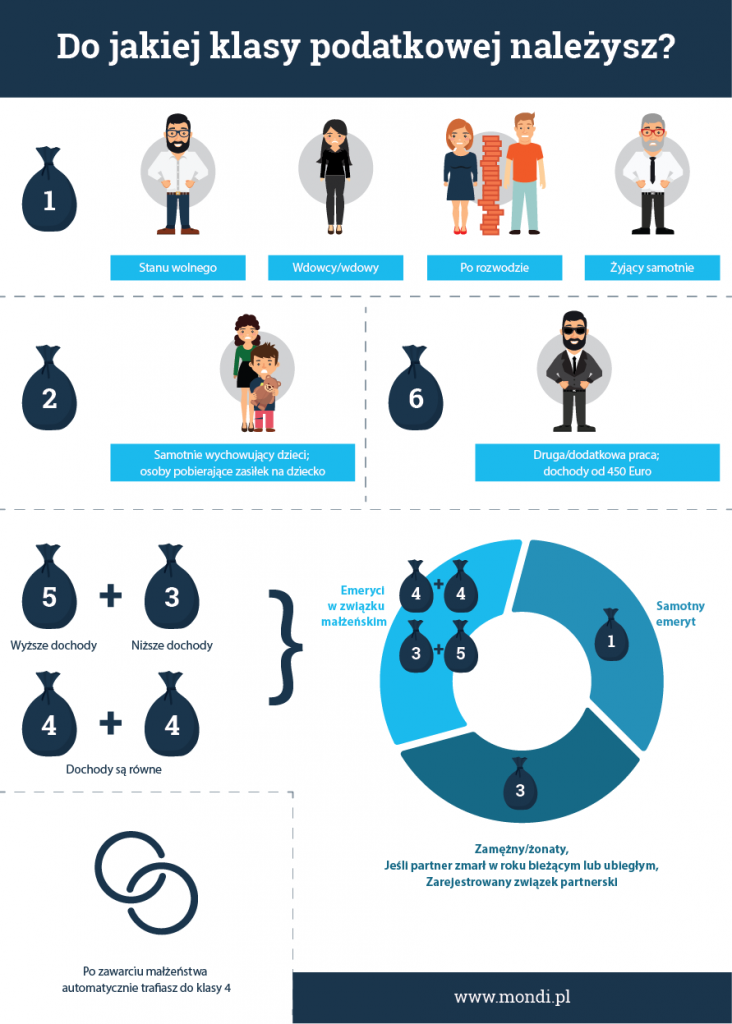

Class 1 – this is where unmarried people are classified – single, married, divorced and widowed. Exceptions are those who fall into Classes II and III.

Class 2 – single persons. This tax class is assigned to unmarried persons and to divorced and widowed persons with at least 1 minor child registered with them. This class includes persons who receive child benefit, guardian’s allowance or Kindergeld. Widowed persons can only belong here if they have not previously been in class III.

Class 3 – these are married persons if the partner is unemployed or not in tax class 5, married persons if the spouse is in a European Community country, and widowed persons during the calendar year.

Class 4 – this tax class is assigned to married persons living together if one spouse is in Class IV.

Class 5 – people whose spouse is in tax class 3 can be accounted for in this tax class.

Class 6 – this class includes people who are employed by more than one employer at one time. Working for two employers at one time qualifies one for this class. This tax class is also granted when there is a discrepancy between the data in the tax authorities and when there is no registration in a particular authority.